Blue Ocean Strategy® Step #4 is all about what’s next: Getting the Strategic Sequence Right.

My hope at this point is that you have already begun your Blue Ocean Strategy® exploring, that you have tackled your strategic canvas for today’s business, and that you are beginning to see new markets emerging before you. Maybe you have even had an adrenaline surge in the brain, that “aha” moment that is telling you that a “big idea” is blasting through. (Note: Usually people fall in love with the idea but run away from ways to turn it into a business that can generate real value for new and existing customers, as well as for their own company.)

Let me explain how Blue Ocean thinking reverses everything.

First, your traditional way of thinking about strategy is totally going to be inverted. Since you are trying to create demand in a new market, you have to shift the focus into new directions. It’s hard to tackle the competition and worry about market share. You have to create demand.

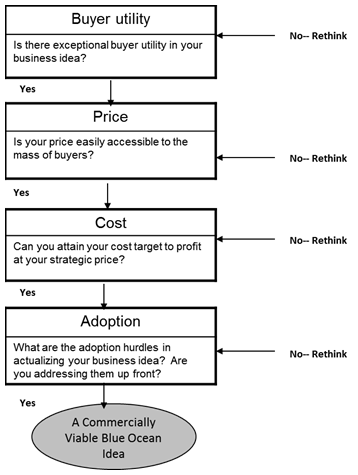

Take your idea, or ideas, and test their usefulness, or utility, for the buyer.

…not for your company but for those who are going to be using your new product or service. You are looking for a mass of buyers who are going to love the new idea you are developing because it:

- Makes their jobs easier or simpler

- Removes the complexity along the entire buying cycle

- Makes them more productive

- Reduces the risk

- Increases the fun or adventure

- Is environmentally friendly

How does your new idea open up a market by eliminating the pain people, your future buyers, have felt in trying to do something?

Or maybe you are ready to add new value in an innovative, creative way? If so, you are on to something. If not, go back and think again. “More of the same but cheaper” is not what this is all about.

Second, change the pricing strategy.

Rather than think “cost + = price,” go backwards. Reverse this process as well. Start with price. At what price point can you open a new market space (preferably a mass market space), thereby creating demand for your idea because of its simplicity, or the way it improves user’s productivity, or its ability to turn something functional into something fun? Most likely, you will need to test this on target markets in clever ways since they will not yet have grasped the value of your new idea.

When Yellow Tail wine entered the market to lure non-wine drinkers to their new label, they priced a bottle at the $6.99 level — about the same as a premium beer, not a budget wine. They were appealing to beer drinkers, not wine drinkers, so their pricing was crucial. They wanted Bud drinkers to trade up to Yellow Tail wine when they were having a party, not to Bass or Guinness. What’s the equivalent for your big idea?

Third, once you have your pricing strategy, tackle the unnecessary costs so you can get to your margin.

Where are these? All too often, they’re hiding in an over-built product that has unnecessary complexity or technological add-ons that really don’t add value. While it might seem a long time ago, Ford’s story is still relevant. When Ford built the Model T, he reversed everything that was being designed for custom cars and wealthy buyers and created a simple (black only) car for the masses. What is the equivalent for your product or service? Have you over-designed it? Have you invested too heavily in the materials going into it, or in the sacred area of customer service? Observe how Southwest Airlines makes the traveling experience completely different for their passengers (starting with free baggage) by taking away complexity and making flying more fun.

Finally, the adoption hurdles are critical to your success.

These are as likely to be your current distributors or clients as your internal staff. As you go through your process of developing your strategy, begin with a serious look across the buying cycle of who is going to say “no, that’s not how we do it.” For many of my clients, one of the first adoption hurdles was their distributors — in their minds, their “clients.” To start with, they realized their distributors were no longer distributing their traditional products in the classic way. They were buying less and less inventory, signaling that they might not be the right conduit for opening a new market space. Or, even if they might be, they probably wouldn’t embrace the changes and lead the charge. Remember that even liquor and wine stores turned away from Yellow Tail before they realized this “non-wine wine” was attracting entirely new non-wine drinkers to their stores.

Interestingly, often the biggest adoption hurdle for these clients was their own team.

Employees are often resistant to change, reluctant to risk their jobs by changing the business model, and uncomfortable with new ideas that point a company in new directions. In building a Blue Ocean market, getting alignment is as important as getting traction.

If your people want to swim in a Red Ocean, you might not want to swim with them.

There is always risk — risk in trying new things and risk in standing still. For innovation to truly happen, your entire team has to participate in creating the changes you are envisioning, and in so doing, metamorphose from Red Ocean dippers into Blue Ocean swimmers.